Apple’s services business has caused a long-time, thoughtful bull to hesitate. Morgan Stanley’s Katy Huberty still thinks that Apple stock is a buy. However, she has lowered her price target on concerns over how richly services should be valued.

Ms. Huberty now believes that Apple shares can climb to $156, for a more modest 23% upside opportunity to mid-Tuesday price levels. This figure compares to nearly 40% gains for the most bullish analysts on Wall Street and Katy’s own 35%, as of roughly four weeks ago.

Figure 1: Morgan Stanley on Apple services.

Apple’s Services: better than expected

What is interesting about Morgan Stanley’s services-driven price target cut is that it comes alongside a positive read on the business itself. According to Seeking Alpha:

“Katy Huberty raises Apple’s Services revenue estimates to account for accelerating Google traffic acquisition cost-related revenue growth and strong App Store revenue. The firm expects Services revenue growth to accelerate by 6 points to 22% year-over-year in FY21, up from the prior 19% year-over-year growth estimate.”

In plain English, the analyst believes that Apple’s service revenues will not only be better than Wall Street’s expectations in 2021 and 2022, but they will also beat her own prior estimates.

The two key pieces of the puzzle are Alphabet’s success (the Mountain View-based company pays Apple billions of dollars per year to be the default search engine) and a positive read on App Store activity in fiscal second quarter.

De-risking valuation expectations

But of course, the devil is in the details. Despite optimism about services, Morgan Stanley points out that valuations (that is, how much the market is willing to pay for the business) have come down so far this year.

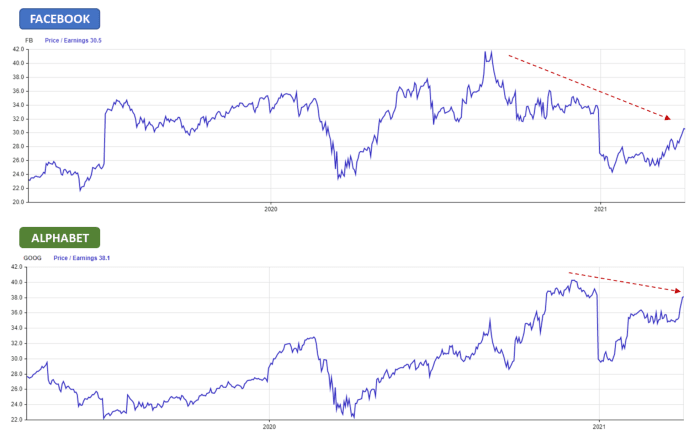

The chart below provides a good depiction of what has been happening. Notice that Facebook’s and Alphabet’s price-to-earnings ratios have been shrinking lately, despite both companies being fundamentally on strong footing. Apply a comparable valuation multiple haircut to Apple’s services segment, and one can begin to understand Morgan Stanley’s modest price target drop on Apple stock.

Facebook and Alphabet P/E.

It is interesting to notice that Apple shares did not sell off on the “taming of the bull”. Quite the opposite: within half an hour of the trading session, on April 6, Apple had been performing better than the Nasdaq and the S&P 500 by about 25 to 50 basis points.

If anything, investors seem to have brushed off Morgan Stanley’s valuation concerns and embraced optimism over better-than-consensus service revenues.

More service optimism

Morgan Stanley was not the only research shop to publish a note on April 6. On the same topic of Apple’s services, Cowen also blew into the bullhorn.

Analyst Krish Sankar sees News+ as “a key pillar in Apple’s subscription business” – one that can “grow from $1 billion in revenue in fiscal 2020 to $2.2 billion by fiscal 2023”. By my estimates, assuming that this prediction comes to fruition, News+ would become a larger business in two years than Apple TV+ is today.

Apple itself has provided more clues that 2021 could be the year of services. In early April, the Cupertino company announced Apple Arcade’s “biggest expansion yet, growing its award-winning catalog to more than 180 games”.

Arcade is yet another offering that can help to add fuel to the fire within Apple’s promising and highly profitable services division.

Twitter speaks

On Monday, April 5, I asked Twitter about what could drive Apple stock to $175 per share – the most optimist price target on Wall Street currently. Surprisingly to me, the services segment was cited as a key factor, slightly ahead of “killer iPhone 12 sales”. Below are the poll results:

Read more from the Apple Maven:

(Disclaimers: this is not investment advice. The author may be long one or more stocks mentioned in this report. Also, the article may contain affiliate links. These partnerships do not influence editorial content. Thanks for supporting The Apple Maven)

Halving Is Here, and With It a Giant Surge in Transaction Fees")